[ad_1]

Even if buyers had been biting their nails forward of the January FOMC choice, that didn’t prevent asset categories and primary currencies from chalking up notable strikes forward of the top-tier match.

Right here’s how markets fared.

Headlines:

Australia This autumn 2024 CPI: 0.2% q/q (0.3% forecast, 0.2% earlier); Headline CPI at 2.5% y/y (2.5% anticipated, 2.3% earlier); Trimmed imply CPI at 0.5% q/q (0.6% forecast, 0.8% earlier)

Jap client self assurance index in January: 35.2 (36.6 forecast, 36.2 earlier)

In his Senate affirmation listening to, Trump’s Trade Secretary select Howard Lutnick mentioned that upper price lists on Canada and Mexico don’t seem to be a carried out deal

American Petroleum Institute (API) estimated that crude oil inventories within the United rose by means of 2.86 million barrels for the week finishing January 17

German GfK client self assurance index in January: -22.4 (-20.5 forecast, -21.4 earlier)

Spanish flash GDP in This autumn 2024: 0.8% q/q (0.6% anticipated, 0.8% earlier)

U.S. items industry stability in December: -122.1B USD (-105.6B USD anticipated, -103.5B USD earlier)

EIA crude oil inventories rose by means of 3.5M barrels (2.2M forecast, -1.0M earlier)

Financial institution of England Governor Bailey reiterated significance of elevating the expansion charge of the economic system

Financial institution of Canada minimize rates of interest by means of 0.25% as anticipated from 3.25% to three.00%; no forecast on long term charge strikes however diminished GDP forecast to at least one.8%; sees price lists as attainable gasoline for power inflation

Fed saved rates of interest on grasp from 4.25% to 4.50% as anticipated, adjusted reliable remark to replicate extra upbeat view on inflation and employment

Fed Chairperson Powell dampened hopes of a March minimize throughout the presser, reiterating that they aren’t in a rush to ease

New Zealand industry stability in Dec: 219M NZD (-1363M NZD forecast, -435M NZD earlier); exports rose 995M NZD whilst imports climbed 404M NZD

Huge Marketplace Value Motion:

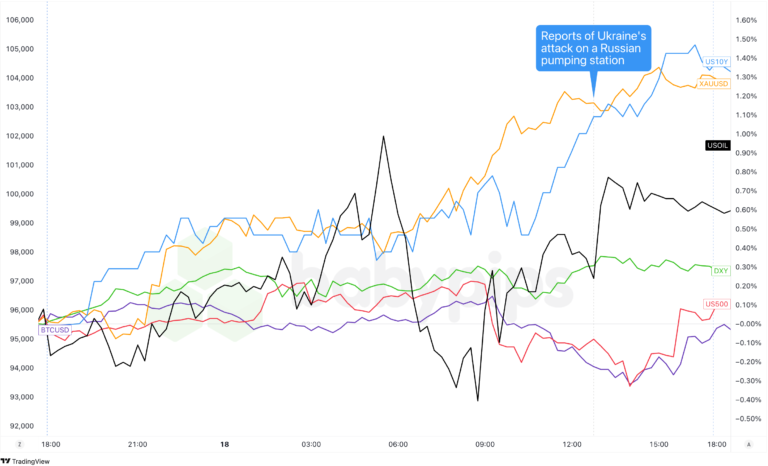

Greenback Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by means of TradingView

The standard possibility correlations had been out of sync early on, as buyers reacted to particular person asset catalysts whilst looking ahead to the the most important FOMC announcement later within the day.

Crude oil confronted important drawback drive all through the day, shedding floor after Trump’s Trade Secretary select Howard Lutnick mentioned that upper price lists on Mexico and Canada will also be have shyed away from in the event that they take motion on unlawful migration and fentanyl flows, slightly discovering reinforce from a less than anticipated construct in API inventories.

Later within the day, the Division of Power’s reliable crude oil stock document confirmed a bigger than anticipated build up of three.5 million barrels as opposed to the sooner relief of one million barrels, sending costs additional south forward of the Fed choice.

Treasury yields, then again, were cruising upper main as much as the FOMC announcement, which then brought about the latter to opposite some features prior to the top of the consultation. Nonetheless, the shorter finish of the yield curve edged upper on dampened expectancies of a March minimize, with the 2-year yield up 1.5 foundation issues to 4.219%.

U.S. fairness indices, which had already been cruising decrease prior to the massive match, pulled relatively upper prior to the shut. Alternatively, this used to be now not sufficient to drag the S&P again within the black because it closed 0.47% decrease for the day whilst the Dow used to be 0.31% within the crimson.

Gold costs confirmed resilience in spite of the more potent buck, whilst BTC/USD endured its spectacular rally, pushing above $103,000 as crypto markets looked as if it would brush aside the Fed’s slightly hawkish stance.

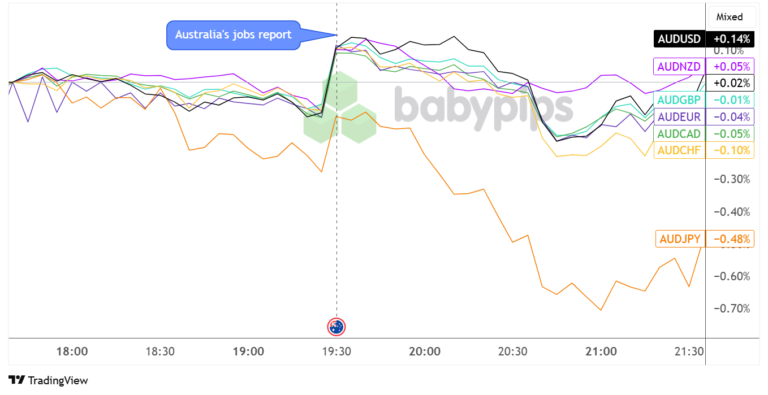

FX Marketplace Habits: U.S. Greenback vs. Majors:

Overlay of USD vs. Main Currencies Chart by means of TradingView

The buck demonstrated important volatility all through the consultation, influenced by means of each home and global components. Early buying and selling noticed the dollar gaining floor towards the Australian buck after the Land Down Below reported a weaker than anticipated CPI that upped the percentages of an RBA minimize quickly.

Main pairs confirmed higher task throughout the London consultation, with the buck widely strengthening as buyers located for a doubtlessly hawkish Fed stance. Alternatively, the momentum shifted as U.S. markets opened, with the buck trimming features because the FOMC assembly approached.

Previous to the Fed match, the Financial institution of Canada diminished borrowing prices by means of 0.25%, resulting in slightly of Loonie weak spot as a result of price lists considerations doubtlessly weighing on expansion possibilities and preserving the central financial institution on its easing cycle.

The Federal Reserve’s choice to handle charges first of all brought on a buck rally, as buyers most probably zoned in on a few hawkish adjustments within the remark, however those features had been in large part reversed throughout Powell’s next press convention.

By means of consultation’s finish, the buck closed marginally upper towards majority of its friends, with some weak spot towards the British pound (-0.08%) and the Jap yen (-0.19%), logging within the most powerful features as opposed to the Australian buck (0.29%).

Upcoming Doable Catalysts at the Financial Calendar:

French flash GDP at 6:30 am GMT

Swiss industry stability at 7:00 am GMT

German import costs at 7:00 am GMT

Swiss KOF financial barometer at 8:00 am GMT

Spanish flash CPI at 8:00 am GMT

German initial GDP at 9:00 am GMT

Eurozone initial GDP at 10:00 am GMT

Ecu Central Financial institution financial coverage choice at 1:15 pm GMT

U.S. advance GDP at 1:30 pm GMT

ECB press convention at 1:45 pm GMT

Tokyo core CPI at 11:30 pm GMT

Jap initial business manufacturing at 11:50 pm GMT

Jap retail gross sales at 11:50 pm GMT

The highlight shifts to the euro space as of late, because the area is because of unlock a handful of initial expansion and inflation figures only some hours forward of the highly-anticipated ECB financial coverage remark.

After that, we’ve were given the U.S. advance GDP studying for This autumn 2024, which might underscore the Fed’s slightly hawkish remark and most probably motive further volatility within the markets.

Don’t omit to take a look at our emblem new the Forex market Correlation Calculator when taking any trades!

[ad_2]

Supply hyperlink