[ad_1]

Uncover the basics of blockchain era on this complete information. Learn the way blockchain works, its key parts, sorts, advantages, real-world programs, and long term doable in reworking industries.

Uncover most sensible fintech information and occasions!

Subscribe to FinTech Weekly’s e-newsletter

Learn via executives at JP Morgan, Coinbase, Blackrock, Klarna and extra

Shariah-compliant finance is a values-driven selection to standard banking and funding programs. Rooted in Islamic regulation (Shariah), this monetary gadget promotes equity, transparency, and risk-sharing whilst adhering to spiritual and moral ideas.

On this complete information, we will delve into the rules, key merchandise, contemporary marketplace developments, and technological inventions shaping the way forward for Islamic finance.

Core Rules of Shariah-Compliant Finance

The basis of Shariah-compliant finance rests on a couple of key ideas designed to make sure equity, transparency, and moral behavior. One of the crucial important facets is risk-sharing, which guarantees that each events interested by a monetary transaction proportion the potential of cash in and loss. This differs from standard finance, the place lenders continuously shift all menace to the borrower via interest-based contracts. In Islamic finance, this equitable distribution prevents exploitation, encourages moral partnerships, fosters transparency, and helps investments in genuine financial actions. It additionally complements monetary steadiness and fosters social justice via making sure that earnings and losses are rather shared.

Prohibition of Riba (Pastime)

Incomes or paying curiosity is precisely forbidden in Islamic finance. As an alternative, cash in is generated via fairness participation, asset-backed transactions, or buying and selling. This concept aligns with risk-sharing, as monetary establishments will have to actively take part within the dangers of investments fairly than incomes assured curiosity.

Chance-Sharing Contracts

Chance-sharing contracts are on the center of Shariah-compliant finance, reflecting the core Islamic concept of equitable distribution of wealth and accountability.

Two number one kinds of risk-sharing contracts facilitate partnerships the place capital suppliers and marketers proportion earnings and losses in share to their contributions:

Mudarabah: A partnership the place one birthday celebration supplies capital whilst the opposite manages the industry. Income are shared according to an agreed ratio, whilst losses are borne via the capital supplier except brought about via negligence.

Musharakah: A three way partnership the place each events give a contribution capital and proportion earnings and losses proportionally, encouraging shared accountability and partnership.

Asset-Subsidized Financing

Transactions will have to be tied to tangible property or products and services to keep away from hypothesis and advertise genuine financial job. This additionally guarantees each events have a vested curiosity within the good fortune of the transaction.

Prohibition of Gharar (Over the top Uncertainty)

Contracts will have to be clear, with obviously outlined phrases and stipulations to attenuate uncertainty. This concept reinforces risk-sharing via making sure all events absolutely perceive the dangers concerned.

Moral Investments (Halal Financing)

Funding is proscribed to companies that conform to Islamic moral requirements, with the exception of industries akin to alcohol, playing, and beef manufacturing. By means of making an investment in moral ventures, each monetary establishments and buyers proportion the ethical accountability and monetary dangers in their actions.

Zakat (Charitable Giving)

A compulsory charitable contribution of two.5% of 1’s wealth, continuously facilitated via monetary establishments, guarantees that wealth is redistributed rather and helps social welfare. A realistic instance of zakat within the context of Shariah-compliant finance may just contain a Shariah-compliant funding fund:

Believe a person has invested in a Shariah-compliant mutual fund specializing in moral industries, akin to renewable power or halal meals manufacturing. On the finish of the fiscal yr, after calculating their general wealth—together with returns from the fund, financial savings, and different property—the investor unearths they’ve a web wealth of $100,000.

Consistent with Islamic ideas, they’re obligated to pay 2.5% zakat on their qualifying property. This quantities to $2,500. Many fiscal establishments providing Islamic finance merchandise facilitate this procedure via providing computerized zakat calculators or immediately managing the cost via distributing price range to qualified charitable organizations. Those organizations most often focal point on poverty alleviation, training, healthcare, or different socially really useful reasons.

On this state of affairs, no longer handiest is the investor’s wealth purified via zakat, nevertheless it additionally contributes to the wider social welfare gadget, supporting the ones in want, which aligns with the moral foundations of Islamic finance.

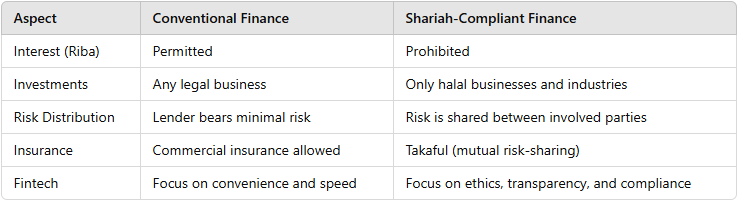

Standard Finance vs. Shariah-Compliant Finance

Key Sectors in Shariah-Compliant Finance

Shariah-compliant finance spans quite a lot of sectors, each and every adapted to fulfill the various wishes of people, companies, and establishments whilst adhering to Islamic moral tips. From private banking answers to state of the art fintech inventions, each and every sector performs a an important function in selling equity, transparency, and accountable monetary practices.

We will be able to discover 4 primary pillars of Shariah-compliant finance: banking, investments, industry financing, and monetary era (fintech).

Shariah-Compliant Banking

Islamic banking gives moral choices to standard banking, adhering to the foundations discussed above. There are two primary varieties of accounts:

Present Accounts: Price range are hung on a believe foundation and are repayable on call for with none returns.

Financial savings Accounts: Perform below Mudarabah agreements, the place earnings are shared between the depositor and the financial institution according to an agreed ratio.

Not unusual banking merchandise come with:

Murabaha (Price-Plus Financing): The place the financial institution buys an asset and sells it to the buyer with a pre-agreed markup.

Ijara (Leasing): The financial institution rentals an asset to the buyer, with possession moving upon contract of entirety.

Qard Hasan (Benevolent Loans): Pastime-free loans equipped for charitable or social reasons.

Shariah-Compliant Investments

Investments in Islamic finance focal point on moral, accountable ventures. An important focal point is on Shariah-compliant shares, which can be stocks of businesses adhering to Islamic moral requirements. Those shares exclude companies interested by industries like alcohol, playing, and beef manufacturing.

A few of the shariah-compliant investments we will to find:

Fairness Investments: Simplest Shariah-compliant shares of businesses that meet explicit moral and monetary standards are authorised.

Sukuk (Islamic Bonds): Structured as asset-backed securities, permitting buyers to earn earnings from the earnings generated via underlying property.

Islamic Mutual Price range: Swimming pools of price range invested in assorted portfolios comprising Shariah-compliant shares and different permissible property.

Traders continuously depend on Shariah screening processes to make sure compliance, which comes to comparing each industry actions and monetary ratios to qualify as Shariah-compliant shares.

Industry Financing in Islamic Finance

Within the realm of Islamic finance, industry financing is structured to align with the core ideas of equity, risk-sharing, and moral funding. In contrast to standard monetary programs, which continuously depend on interest-based loans, Islamic industry financing mechanisms make sure that each the financier and the entrepreneur proportion the dangers and rewards of the undertaking. This fosters larger collaboration, monetary inclusion, and long-term sustainability for companies, irrespective of their dimension.

Mudarabah (Benefit-Sharing Partnerships)

Mudarabah is a monetary partnership the place one birthday celebration supplies the capital (known as rab al-mal) and the opposite gives managerial experience and hard work (the mudarib). This association is especially well-suited for startups, small companies, and marketers who would possibly not have the capital to release their ventures however possess the abilities and innovation mandatory for industry good fortune.

On this contract, earnings generated from the industry actions are shared between the 2 events in keeping with a pre-agreed ratio. As an example, an investor may obtain 70% of the earnings, whilst the entrepreneur keeps 30%. Then again, if the industry incurs losses, they’re borne only via the capital supplier except the loss is because of negligence or mismanagement via the entrepreneur. The entrepreneur’s loss, on this case, could be the effort and time they invested within the undertaking.

This construction encourages marketers to innovate and attempt for industry good fortune with out the force of debt reimbursement, whilst buyers can diversify their portfolios with alternatives that align with Islamic moral requirements.

Musharakah (Joint Ventures)

Musharakah is every other very important monetary association in Islamic finance, emphasizing joint possession and mutual cooperation. In contrast to Mudarabah, the place just one birthday celebration provides capital, Musharakah comes to all companions contributing capital, effort, or each. All events proportion earnings and losses proportionally to their respective investments except in a different way agreed upon.

This style is extremely versatile and can also be carried out in quite a lot of industries, from genuine property construction to large-scale commercial tasks. As an example, two firms may input a Musharakah settlement to finance a brand new manufacturing unit, each and every contributing 50% of the specified capital. Income from the manufacturing unit’s operations would then be allotted similarly or in keeping with a unique mutually agreed ratio.

The construction of Musharakah incentivizes all companions to actively take part in industry operations since everybody has a vested curiosity within the undertaking’s good fortune. This guarantees that capital is applied successfully, and menace is sent rather amongst all stakeholders.

Murabaha (Industry Financing)

Murabaha is without doubt one of the maximum not unusual financing gear in Islamic finance, in particular helpful for business and asset acquisition. As an alternative of offering a right away mortgage, the financial institution or monetary establishment purchases items or property on behalf of a consumer after which sells them to the buyer at a pre-agreed markup.

For example, a small industry wanting new equipment would possibly means an Islamic financial institution for financing. The financial institution will acquire the equipment immediately from the provider after which promote it to the industry proprietor at a cost-plus-profit worth. The entrepreneur can then pay off the financial institution in installments over an agreed length.

In contrast to standard loans, which contain curiosity bills, Murabaha transactions are according to clear, in advance agreements about cash in margins. This style removes uncertainty for each events, because the phrases are obviously outlined, and it guarantees compliance with Shariah ideas via linking the transaction to a tangible asset.

Salam Contracts (Advance Fee Financing)

The Salam contract is a ahead settlement during which a purchaser will pay for items or products and services prematurely, with supply scheduled for a long term date. This association is especially really useful in agricultural financing, the place farmers continuously want price range sooner than harvest to hide manufacturing prices.

Beneath a Salam settlement, a monetary establishment supplies price range in advance to a farmer for the cultivation of plants like wheat or dates. In go back, the farmer commits to handing over a specified amount of the crop at an agreed-upon time sooner or later. The associated fee is most often set not up to the anticipated marketplace worth on the time of supply, providing an incentive for early financing whilst offering safety for each events.

This style serves as a type of operating capital financing for manufacturers, making sure they’ve the liquidity had to meet manufacturing prices. It additionally is helping stabilize marketplace costs via securing gross sales sooner than the harvest, thereby lowering uncertainty for each manufacturers and patrons.

Really useful studying:

Inventions in Shariah-Compliant Fintech

Shariah-compliant fintech is taking part in an more and more necessary function in making Islamic monetary merchandise extra obtainable, environment friendly, and clear. By means of merging complex applied sciences with the moral and risk-sharing ideas of Islamic finance, fintech answers are serving to to bridge gaps in monetary inclusion and democratize get entry to to Shariah-compliant monetary products and services.

Those inventions no longer handiest simplify complicated monetary transactions but in addition supply buyers and companies with gear that ensure that complete compliance with Islamic regulation. Right here’s an in depth have a look at one of the most maximum impactful applied sciences reshaping Shariah-compliant finance.

Crowdfunding Platforms

Crowdfunding has emerged as an impressive instrument for financing moral ventures in keeping with Islamic ideas. Shariah-compliant crowdfunding platforms perform according to contracts akin to Mudarabah (profit-sharing) and Musharakah (joint ventures), permitting people to pool price range for tasks whilst sharing earnings and losses rather.

As an example, an entrepreneur looking for to release a halal meals industry can elevate price range via a crowdfunding platform with out enticing in interest-based debt. Traders give a contribution capital in trade for a proportion of the earnings, which is pre-agreed upon via a Mudarabah association. However, in a Musharakah construction, all individuals proportion possession within the industry and take part in decision-making.

Those platforms advertise inclusivity via enabling small buyers to take part in moral ventures and giving startups get entry to to much-needed investment with out violating Shariah ideas.

Peer-to-Peer Lending (Qard Hasan)

Peer-to-peer (P2P) lending has turn into an leading edge method for people and companies to get entry to investment with out the desire for standard monetary intermediaries. Within the context of Islamic finance, P2P lending most often follows the Qard Hasan style, which gives interest-free loans to these in want.

On this association, lenders supply price range with out anticipating monetary returns, and debtors are obligated to pay off handiest the most important quantity. This style is especially helpful for small companies, marketers, and people looking for monetary aid with out falling into debt traps brought about via interest-bearing loans.

Platforms facilitating Qard Hasan loans intention to advertise monetary inclusion, particularly for underserved populations, via providing moral monetary reinforce according to mutual help and neighborhood harmony.

Blockchain Era

Blockchain era is revolutionizing Islamic finance via bettering transparency, safety, and potency. One in all its maximum promising programs is within the issuance of sukuk (Islamic bonds). Historically, issuing sukuk comes to complicated documentation and a couple of intermediaries, which can also be expensive and time-consuming.

Blockchain streamlines this procedure via making a decentralized, immutable ledger of transactions. Each step of the sukuk issuance—possession switch, cash in distribution, and compliance tracking—can also be recorded securely at the blockchain. This reduces transaction prices, will increase transparency, and minimizes the danger of fraud or manipulation.

A number of nations, together with Bahrain and Malaysia, have already began exploring blockchain-based sukuk issuance as a method of fostering innovation in Islamic finance whilst keeping up strict compliance with Shariah ideas.

Robo-Advisory Platforms

Robo-advisory platforms are reworking how people put money into Shariah-compliant shares and different monetary tools. Those virtual platforms use algorithms and AI-driven gear to supply computerized, customized funding recommendation according to person personal tastes, menace tolerance, and monetary objectives—all whilst making sure strict adherence to Islamic monetary tips.

A person occupied with construction a halal funding portfolio can use a robo-advisory provider to routinely clear out non-compliant property, akin to shares from firms interested by playing, alcohol, or interest-based monetary establishments. The platform regularly rebalances the portfolio to take care of compliance with Shariah screening standards.

Platforms like Wahed Make investments have won world reputation for making moral making an investment extra obtainable, particularly for more youthful buyers preferring virtual answers over conventional monetary advisors.

AI-Based totally Zakat Calculators

Zakat, or obligatory charitable giving, is a an important pillar of Islamic finance. Calculating zakat generally is a complicated procedure, because it comes to assessing wealth throughout quite a lot of asset categories, together with money, gold, industry source of revenue, and investments.

AI-based zakat calculators simplify this procedure via automating calculations according to real-time monetary knowledge. Customers enter their property and liabilities, and the gadget routinely determines the right kind zakat quantity due, making sure complete compliance with Islamic regulation.

Some complex platforms even be offering computerized cost distribution to eligible charities, making it more uncomplicated for customers to satisfy their spiritual duties whilst supporting social welfare projects.

Marketplace Developments and Enlargement Knowledge

Fresh years have noticed important enlargement within the Islamic finance business:

The worldwide Islamic finance marketplace is projected to develop from $3.49 trillion in 2024 to $5.75 trillion via 2034, at a CAGR of five.13%.

Sukuk issuances reached $46.8 billion via March 2024, up from $38.2 billion in 2023.

MENA stays the dominant marketplace, whilst the Asia-Pacific area is experiencing speedy enlargement.

The AAOIFI has presented stricter rules for sukuk issuances, making sure higher investor coverage.

In the United Kingdom, Shariah-compliant pension price range have grown considerably, with 30% returns and asset enlargement of £180 million in state-backed schemes like Nest.

The call for for Shariah-compliant shares is emerging as extra buyers search moral funding alternatives aligned with Islamic ideas.

Demanding situations and Long run Outlook

The Islamic finance sector faces a number of demanding situations:

Regulatory Complexity: Other interpretations of Shariah compliance throughout jurisdictions.

Training and Consciousness: Many buyers lack working out of Islamic finance ideas.

Technological Scalability: Enforcing fintech answers whilst making sure compliance with Shariah regulations.

In spite of those demanding situations, the long run appears promising with:

Enlargement into untapped markets in Africa and Central Asia.

Integration with ESG (Environmental, Social, and Governance) frameworks.

Greater use of AI and blockchain to beef up transparency and potency.

As world curiosity in moral making an investment grows, the call for for Shariah-compliant shares is predicted to upward push, attracting each Muslim and non-Muslim buyers.

Conclusion: Why Shariah-Compliant Finance Issues

Shariah-compliant finance gives a novel, moral method to monetary control. It emphasizes equity, transparency, and social accountability, making it horny for each Muslim and non-Muslim buyers looking for accountable monetary answers. With sturdy enlargement projections, emerging call for for Shariah-compliant shares, and ongoing technological developments, Islamic finance is poised to play a pivotal function in shaping the way forward for world finance.

[ad_2]

Supply hyperlink